Entries with label .

It generates many of the raw materials needed for global technology production.

China not only has significant reserves of mineral resources, but also leads the world in the production of many of them. B This gives it a geopolitical advantage as source of the resources essential for global technological production.

▲Satellite image [NASA].

article / Gabriel Ros Casis [English version].

With such a vast territory as the Asian country, it is obvious to think that it possesses a large amount of raw materials and natural resources. Throughout China's history, this has become a strong geopolitical asset, not only for the country's own development but also for its trading partners through exports. Today, when we talk about these raw materials, China stands out in two main groups: base metals and technological elements.

The group of the base metals essentially comprises five metals from the periodic table, these being: iron, copper, aluminum, magnesium and zinc (sometimes lead and tin are also included). There is no need to recall that we can find all these metals in everyday objects, and that they have been the backbone of industry for a long time. Therefore, every country needs them, placing those with the largest deposits of these metals at a strategic advantage. But a country's mineral wealth is not always given by this condition, as it can also be measured by the ease and feasibility of extracting the product. In the case of China, both arguments would be valid, since the country has the largest deposits of many of these minerals, with magnesium leading the way (79% of global extractions) followed by tin (43%) and zinc (31%).

As far as technological metals are concerned, it is important to note that they include various minerals, such as rare earths, precious metals, as well as semiconductors. From a quantitative approach , the required amount of these metals is minimal, even though their availability is crucial for the production of today's technology. For example, some of the most common technology metals include lithium, yttrium, palladium, cerium and neodymium, which can easily be found in cell phone batteries, medicines, magnets or catalysts. Once again, China leads the way with the largest deposits of several of these elements, especially tungsten (83%), followed by rare earths (78%) and molybdenum (38%).

From this we can conclude that China not only has the largest deposits, but is also the world's leading exporter. In addition to extraction, this country also refines and manufactures components with minerals such as aluminum, copper and certain rare earths, and in some cases even manufactures the final product.

Therefore, it must be taken into account that extraction brings with it certain consequences. Environmentally, extraction always has an impact on the land, perhaps less in China compared to other countries (due to the size of its territory), but equally significant. From an economic approach , these extractions entail a great cost, but which, managed in the right way, can generate an immense benefit. In the political scenario, they are seen as an important geopolitical advantage, creating dependence on the demand of other countries.

As a conclusion, it can be drawn from this that China has great power in terms of raw material resources, but this carries with it a great responsibility, since a substantial part of the raw materials used for almost all the world's technology production depends on this country, which provides the resources, but also manufactures them.

The cycles of the Latin American Economics are closely linked to mineral prices: the graphs are astounding.

Public attention on the price of commodities is often focused on hydrocarbons, preferably oil, because of the direct consequences on consumers. But although Latin America has major crude oil producers, minerals are a more cross-cutting asset on the region's Economics , especially in South America. This is demonstrated by the largely parallel lines that follow the evolution of non-energy minerals and GDP growth, both in times of boom and bust.

article / Ignacio Urbasos Arbeloa [English version].

Mining is a fundamental activity for many Latin American economies. The sector has an enormous weight in exports and foreign investment, making it one of the main sources of foreign exchange. In contrast to the general perception of non-energy mining as a mature industry, the sector continues to be attractive to investors and is capable of continuing to generate employment and wealth. Latin American mining receives 30% of the world's investment in the sector, which expects a recovery in prices. The impact of these fluctuations has direct consequences on the economies of the continent, some of which are highly dependent on the exploitation and sale of these resources. The goal of this analysis is to articulate a convincing explanation of the Degree in which these price variations affect national GDPs.

First of all, it is important to detail the chronological evolution of prices of the main minerals exploited in Latin America. The general trend in commodity prices over the last two decades has been marked by enormous volatility. The so-called commodity super cycle [1] given approximately between 2003 and 2013, with a setback between 2008 and 2009, occurs at the same time as the so-called golden decade in Latin America. This status was produced by an unprecedented rise in world demand, thanks to emerging countries led by China, which has transformed foreign trade in the region, displacing the USA as the first partner of most of these countries.

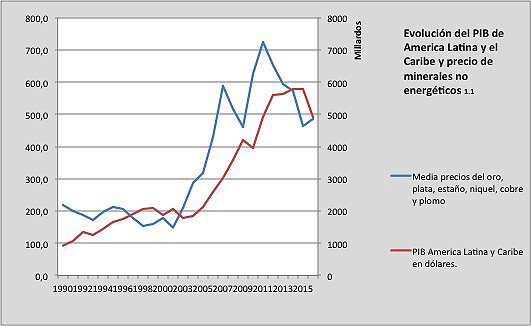

The evolution in prices has followed a very similar patron saint in non-energy mining, which by rule generally follows the price trends of the rest of the raw materials. As we can see in Figure 1.1, the Latin American and Caribbean region has had an economic growth very similar to the average evolution of gold, silver, tin, nickel, lead and copper prices. It is important to mention that the relationship between these two variables is not isolated, and should be analyzed in the above-mentioned context of a general rise in the prices of other raw materials of vital importance for the region, such as hydrocarbons or agricultural products.

|

[The graphs are based on World Bank Data and national statistics from Peru and Chile] [The graphs are based on World Bank Data and national statistics from Peru and Chile]. |

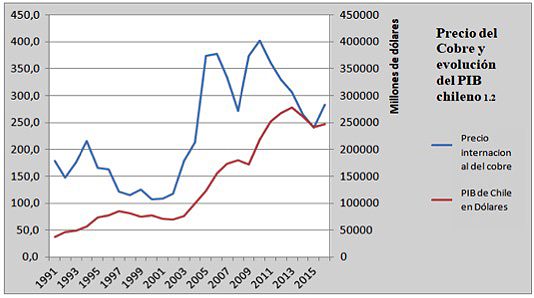

The case of Chile can be extremely useful. Chile has a Economics particularly specialized in non-energy mining, highlighting the exploitation of copper, an activity in which it is a world leader and which accounts for 50% of its exports. The mining sector in Chile [2] reached almost 20% of GDP in the mid-2000s; in 2017 it has accounted for around 9%. In Figure 1.2 we see how the price of copper sets the country's economic path, with the greatest periods of Chilean economic growth coinciding with the increase in copper prices. Despite being one of the most developed economies in the region [3], with a 74% weight of the services sector in GDP, the country is still conditioned by the situation of its primary sector and specifically mining.

|

|

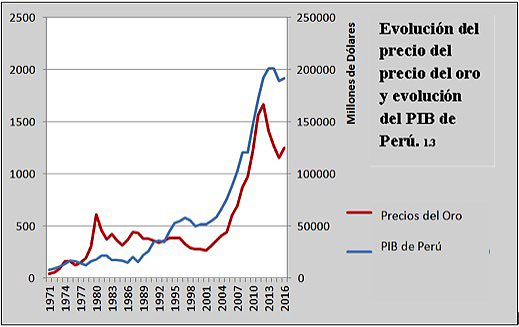

Another interesting case is Peru, a country whose exports include a good share of non-energy minerals [4], reaching 46% of exports in the case of gold (18%) and copper (26%). Similarly to Chile, the share of mining in the Economics is 15% of GDP. Again, we can appreciate the correlation between the prices of certain strategic non-energy minerals and economic growth.

|

|

This relationship is logical and responds to several realities. On the one hand, the great quantitative value of raw materials in Latin American economies, which concentrate their exports in agricultural, mineral and energy products. On the other hand, its qualitative importance since the sector generates large amounts of employment (up to 9% in Chile), is the object of many of the main companies in the region (5 of the 20 largest in Latin America are dedicated to extraction), is the main source of foreign currency and leaves enormous benefits for the coffers of the States, since they are governed under a particular tax system more burdensome. Likewise, a good part of the payment of foreign debt is covered by these revenues, and price instability could bring back the ghosts of the debt crisis of the eighties, something that is already a reality in the case of Venezuela.

Although the countries of Latin America cannot be analyzed as a heterogeneous unit, in general terms the region does face a common challenge : to be able to reduce the dependence of its economies on the exploitation and export of raw materials. An activity that has problematic elements such as its impact on the environment, a particularly complex issue in the region due to the reticence of indigenous groups, or the quality and stability of the employment they generate. In any case, the region's industrial development is still deficient and there are more and more voices warning that the golden decade of 2003-2013 was not used to make the necessary structural changes to mitigate this status [5].

The existence of complex realities partner-politics in Latin America has often led to the use of the benefits derived from extraction in short term and electoral policies, a scourge that increases the exhibition of social welfare to the ups and downs of the mining and energy sector. Although commodity price predictions point to an imminent recovery [6], status is not expected to be similar to the one around 2008 when prices reached historic highs. This new situation will demand the maximum from Latin American economies, which will not be able to count on such a favorable status from the international Economics .