Entries with Categories Global Affairs .

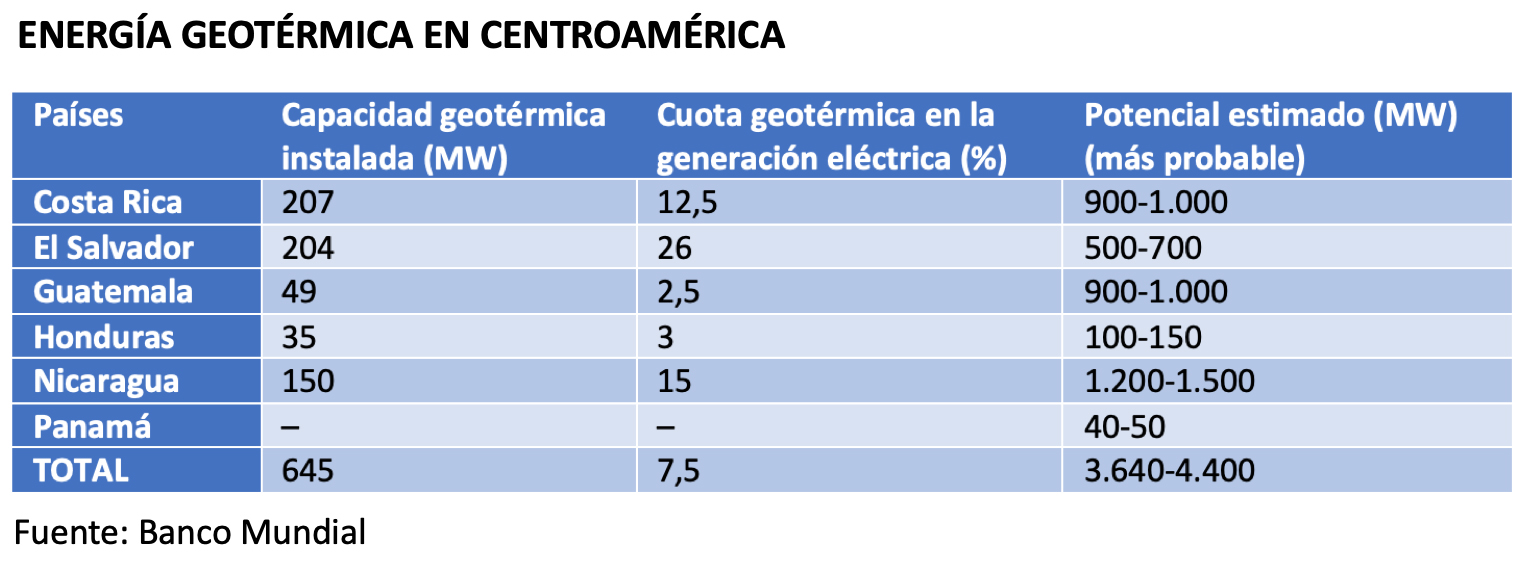

Geothermal energy already accounts for 7.5% of the Central American electricity mix, with installed capacity still far below the estimated potential.

Central America's volcanic activity and tectonic movements offer optimal conditions for the region's small countries to take advantage of an alternative energy source to imported hydrocarbons or an ever more polluting coal. At the moment, the installed capacity -largest in Costa Rica and El Salvador- is barely 15% of the most likely estimated potential.

![San Jacinto-Tizate geothermal power plant in Nicaragua [Polaris Energy Nicaragua S. A.] [Polaris Energy Nicaragua S. A.].](/documents/10174/16849987/geotermica-blog.jpg "San Jacinto-Tizate geothermal power plant in Nicaragua [Polaris Energy Nicaragua S. A.] [Polaris Energy Nicaragua S. A.].")

▲ San Jacinto-Tizate geothermal plant in Nicaragua [Polaris Energy Nicaragua S. A.] [Polaris Energy Nicaragua S. A.].

article / Alexia Cosmello

Central America currently has an installed geothermal capacity of 645 megawatts (MW), far from the potential attributed to the region. This may reach, in the highest band of estimates, almost 14,000 MW, although the most likely estimates speak of around 4,000 MW, which implies a current utilization of approximately 15%, according to data of the World Bank published in 2018.

The energy obtained constitutes 7.5% of the total electricity generation in Central American countries: a not insignificant figure, but one that still needs to grow. Forecasts point to an expanding sector, although attracting the necessary foreign investment has so far been limited by the risks inherent in this industry and national legal frameworks.

Geothermal energy is a clean, renewable energy that does not depend on external factors. It consists of harnessing the heat of the earth's interior - high temperature resources in the form of hot subway fluids - for electrical and thermal generation (heating and domestic hot water). It is governed by the magmatic movement of the earth, which is why it is a scarce resource and limited to certain regions with a significant concentration of volcanic activity or tectonic movement.

Latin America

These characteristics of the American isthmus are also shared by Mexico, where the geothermal sector began to develop in the 1970s and has reached an installed capacity of 957 MW. The friction of the tectonic plates along the South American and eastern Caribbean coast also gives these subregions an energy potential, although less than that of Central America; its exploitation, in any case, is small (only Chile, with 48 MW installed, has really begun to exploit it). The total geothermal potential of Latin America could be between 22 GW and 55 GW, a particularly imprecise range given the few explorations carried out. Installed capacity is close to 1,700 MW.

The World Bank estimates that over the next decade, Latin America would need an investment of between US$2.4 billion and US$3.1 billion to develop various projects, which would add a combined generation of some 776 MW, half of which would correspond to Central America.

Attracting private capital is not easy, considering that since the 1990s the Latin American geothermal sector has had less than US$1 billion in private investment. Financing difficulties are partly related to the very nature of the activity, as it requires a high initial investment, which is high risk because exploration is laborious and it takes time to reach the energy production stage. Other aspects that have made it less attractive have been the policies and regulatory frameworks of the countries themselves and their deficiencies in the local and institutional management .

Geothermal energy, in any case, should be a priority for countries with high potential such as Central America, given that, as the International Renewable Energy Agency (IRENA) points out, it constitutes a low-cost electricity generation source and also stimulates low-carbon economic growth. For this reason this organization has order to the governments of the Central American region to adopt policies that favor the use of this valuable resource , and to develop legal and regulatory frameworks that promote them.

The World Bank and some countries with particular technological expertise are involved in international promotion and advice. Thus, Germany is carrying out since 2016 a program of development of geothermal potential under the German Climate Technology Initiative (DKTI). The project cooperates with the development Geothermal Fund (GDF), implemented by the German development bank KfW, and the Central American Geothermal Resource Identification Program, supported by the German Federal Institute for Geosciences and Natural Resources (BGR). goal The initiative is also supported by the German Agency for International Cooperation (GIZ), which has organized technical courses, together with business LaGeo, located in El Salvador, for geothermal plant operators, teachers and researchers at subject, with the aim of achieving a better management of the installations and a more efficient development of the energy projects.

By country

Although Central American countries have shown a high dependence on imported hydrocarbons as energy source , in terms of electricity generation the subregion has achieved an important development of renewable alternatives, put at the service of all members of the Central American Integration System (SICA) through the Electrical Interconnection System for Central American Countries (SIEPAC). The executive director of the administrative office General of SICA, Werner Vargas, highlighted at the beginning of 2019 that 73.9% of the electricity produced at the regional level is generated with renewable sources.

However, he indicated that in order to cope with the growing electricity demand, which between 2000 and 2013 increased by 70%, the region needs to make greater use of its geothermal capacities. Greater integration of geothermal energy would save more than 10 million tons of CO2 emissions per year.

The share of geothermal energy in the electricity mix varies from country to country. The highest share corresponds to El Salvador (26%), Nicaragua (15%) and Costa Rica (12.5%), while the share is small in Honduras (3%) and Guatemala (2.5%).

In Costa Rica, the Costa Rican Electricity Institute (ICE) delivered last July the Las Pailas II geothermal plant, in the province of Guanacaste, at a total cost of US$366 million. The plant will contribute a maximum of 55 MW to the electric network , so that when it is fully operational it will raise the total installed capacity in the country from 207 MW to 262 MW.

Costa Rica is followed by El Salvador in electricity generation from geothermal energy. The national leader in production is business LaGeo, manager of almost all of the 204 MW installed in the country. This business has two plants, one in Ahuachapá, which produces 95 MW, and the other in Usulután, with a production of 105 MW. With lower electricity consumption than Costa Rica, El Salvador is the Central American country with the highest weight of geothermal generation in its electricity mix, 26%, double that of Costa Rica.

Nicaragua has an installed capacity of 150 MW, thanks to the geothermal interest of the Pacific volcanic mountain range. However, production levels are clearly below, although they account for 15% of the country's electricity generation. Among the geothermal projects, the San Jaciento-Tizate and Momotombo projects are already being exploited. The first one, exploited by business Polaris Energy, was built in 2005 with the initial intention of producing 71 MW, to reach 200 MW by the end of this decade; however, it is currently producing 60 MW. The second, controlled by business ORMAT and the participation of ENEL, was promoted in 1989 with a capacity of 70 MW, although since 2013 it has been producing 20 MW.

Guatemala is slightly behind, with an installed capacity of 49 MW, followed by Honduras, with 35 MW. Both countries recognize the interest of geothermal exploitation, but have lagged behind in promoting it. And yet the Guatemalan government's ownprograms of study highlights the profitability of geothermal resources, whose production cost is US$1 per MW/hour, compared to US$13.8 in the case of hydroelectric power or 60.94 percent for coal.

The upcoming gas self-sufficiency of its two major buying neighbors forces the Bolivian government to look for alternative markets

![Yacimientos Pretrolíferos Fiscales Bolivianos (YPFB) gas plant [Corporación YPFB].](/documents/10174/16849987/bolivia-gasnatural-blog.jpg "Yacimientos Pretrolíferos Fiscales Bolivianos (YPFB) gas plant [Corporación YPFB].")

▲ Yacimientos Pretrolíferos Fiscales Bolivianos (YPFB) gas plant [Corporación YPFB].

ANALYSIS / Ignacio Urbasos Arbeloa

Bolivia, under Evo Morales, is the only economic success story of all the Latin American countries that embraced left-wing populism at the beginning of this century. Together with Panama and the Dominican Republic, Bolivia has achieved the highest GDP growth in the region in the last five years, and all this in a difficult context of decline on the part of its main trading partners: Argentina and Brazil[1]. The political stability brought by Evo Morales since 2006, coupled with prudent counter-cyclical macroeconomic policies and a new hydrocarbons management are part of the formula for this success. Nevertheless, there are enormous economic and political risks for Bolivia. On the one hand, natural gas accounts for 30% of exports and its destination is exclusively Brazil and Argentina, countries that are close to gas self-sufficiency. Finding alternative routes is not an easy task for a landlocked state, with a diplomatic conflict with Chile and separated by the Andes Mountains from Peru. Moreover, the Bolivian government's bid to exploit lithium through national companies that integrate its processing to favor industrialization is a risky strategy that could leave the country out of the growing world lithium market. Finally, Evo Morales and the MAS have followed a growing authoritarian trend, allowing the reelection of the president, undermining the separation of powers and the recent 2009 constitution. The new Bolivia faces in the next decade the challenge of reorienting its natural gas exports, diversifying its Economics and consolidating a real democracy that will allow a sustained growth of its Economics and its role as a regional actor.

Natural Gas: at the center of the 21st century political discussion

During the failed oil explorations in the Chaco in the 1960's, abundant natural gas reserves of great economic potential were found at finding . Although it was a resource of lesser value than crude oil, an incipient gas industry was soon developed by foreign companies, mainly American, such as Standard Oil. In 1972 a first nationalization took place, with the emergence of YPFB as the state-owned business in charge of the exploration, production, transportation and refining of Bolivian energy resources in partnership with foreign companies. That same year, the first export gas pipeline to Argentina was built. By 1999, Bolivia will export natural gas to Brazil through the Santa Cruz-Sao Paulo pipeline, whose project took more than eight years of negotiations and construction work and introduced Petrobras as an important player in the sector. Thus, Bolivia enters the 21st century with a growing gas industry, mostly privatized by the first government of Gonzalo Sánchez de Lozada, and boosted by a very favorable fiscal model for foreign companies[2].

The year 2001 marks the beginning of a convulsive political stage in Bolivia with the so-called Water War. A wave of protests arose from the privatization of municipal water services in the framework of financial negotiations between the IMF and the government of Hugo Banzer. At the nerve center of these protests in Cochabamba emerged the figure of Evo Morales, a coca growers' leader who will increase his popularity unstoppably. Gas became the protagonist in 2003, with a new wave of protests against the construction of a natural gas pipeline from Tarija to Mejillones (Chile) for consumption by the Chilean mining industry and export to Mexico and the USA in the form of LNG. The civil service examination at project argued the historical incoherence of contributing Bolivian resources to the exploitation of the mining region lost to Chile in the War of the Pacific (1879-1883) and which deprived Bolivia of an outlet to the sea. In addition, an alternative, more costly gas pipeline through Peru was proposed, but which would supposedly benefit the northern region of Bolivia and would not be a national humiliation. The protests took a nationalist and indigenist turn and became a real revolution that blocked La Paz, the international airport and plunged the whole country into violence and shortages. President Lozada resigned and most of his government fled abroad, while the project was cancelled and buried forever.

The new president Mesa comes to power with the promise to call for a binding referendum on gas, the establishment of a Constituent Assembly and a reform of the Hydrocarbons Law, including a review of the privatization processes. The referendum ended up giving the victory to Carlos Mesa's proposals, although with a leave participation and a confusing essay of the questions. President Mesa, unable to capitalize on the legitimacy granted by the plebiscite Withdrawal to position and called early presidential elections in 2005, which brought to power the first indigenous president in the history of Bolivia, Evo Morales, with an absolute majority. Natural gas thus became the main catalyst for political change in Bolivia.

Hydrocarbon reform

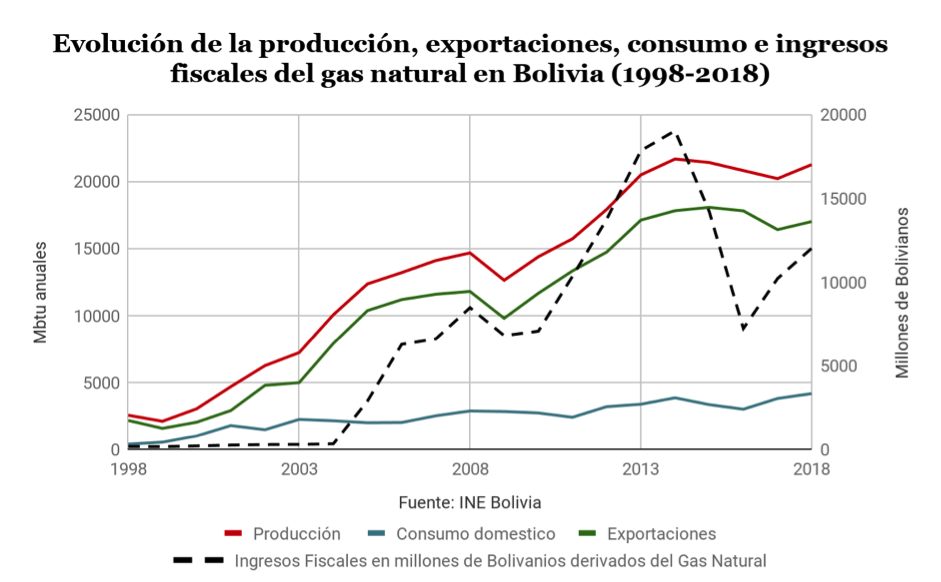

The arrival of Evo Morales brought about a profound change in the hydrocarbons legal framework . In 2006 the new hydrocarbons law "Heroes del Chaco" was enacted, nationalizing Bolivia's energy resources, expropriating 51% of the shares of companies involved in the sector and establishing a direct tax on hydrocarbons of 50% subject to an extra royalty of 32% to YPFB in those fields with more than 100 mcf of annual production[3]. This legislation, in the words of Evo Morales "turned the tables, going from 18% to 82% of the State's income on hydrocarbons"[4]. The legislation, although adorned with a radical revolutionary rhetoric, has proven to be moderate and viable in the medium term, since it allows in the internship much less burdensome tax formulas for energy multinationals and did not imply large expropriations of assets. As can be seen in the graph below, tax revenues from natural gas have grown enormously since 2005, the year of the reform, without dramatically affecting natural gas production. Moreover, this reform was accompanied by record highs in the price of raw materials in 2006, 2007 and 2008, cushioning the percentage reduction in foreign companies' revenues. In 2009 Bolivia included in article 362 the primacy of oil service contracts, a formula in which multinationals do not obtain any rights over the hydrocarbons extracted, but are remunerated for the services rendered.

Since the reform, exports have been relatively stable, buoyed by growing demand in both Brazil and Argentina. The most controversial case occurred in the particularly cold winter of 2016, when Bolivia halted exports due to maintenance work at the Margarita field. This event unmasked a stubborn reality about Bolivia's proven natural gas reserves and the need to increase exploration and drilling work in the country. Bolivia's current reserves amount to 283 bcm (10 tcf), enough for only 10 years of export activity at the current rate. Aware of this status limit, the YPFB corporation has launched an investment campaign for 2019 amounting to 1.45 billion dollars, of which 450 million dollars will be dedicated to exploration work[5]. Much of the investment in the sector in recent years has been aimed at industrializing natural gas production instead of exploration work, building refining plants such as the Bulo Bulo ammonia and urea plant[6]. Total, Shell, Repsol and Petrobras are currently working in exploration and production[7]. This effort is intended to answer the IMF's report , which considered Bolivia's natural gas reserves to be too scarce to turn the country into a regional energy center, Evo Morales' greatest aspiration[8]. For YPFB, there are probable reserves of 850 bcm (35 tfc) that would guarantee a long life for the gas sector, but it should rethink its fiscal policy in order to attract foreign companies, which currently account for only 20% of total investment[9].

The future of Bolivian natural gas

From agreement with the contracts signed with Brazil (1999) and Argentina (2005) export prices are indexed to a basket of hydrocarbons, which in general has guaranteed Bolivia a very favorable price, higher than the Henry Hub, but which makes the country equally dependent on fluctuations in international commodity prices. However, the revolution of non-conventional technology and new forms of transportation, now more economical, such as LNG, are transforming the reality of the natural gas market in the Southern Cone. This new situation, linked to the end of the contracts with Brazil in 2019 and Argentina in 2026, puts in check the future of the main asset of the Bolivian Economics .

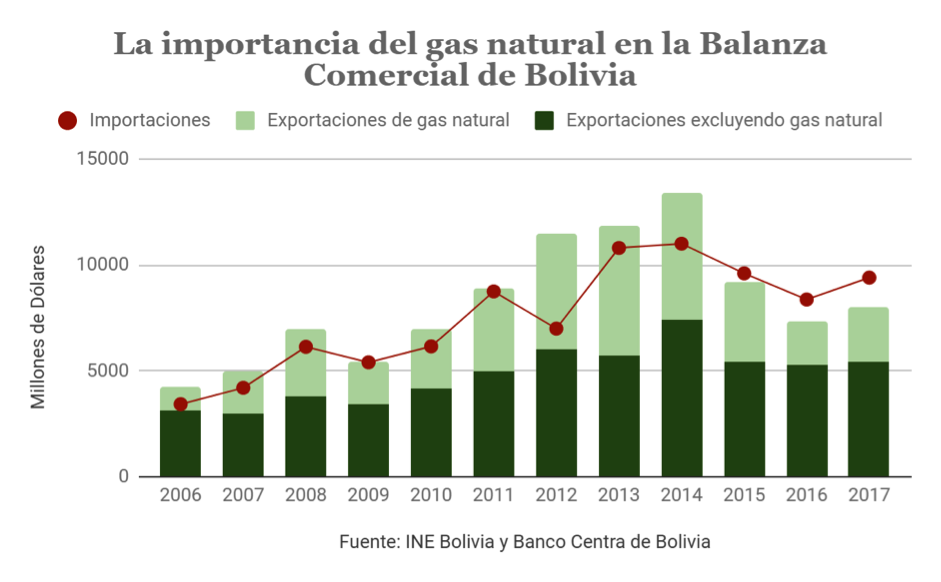

As shown in the graph sample , the Bolivian trade balance and its fiscal stability depend on the exported volumes of natural gas and its international price. The survival of the current Bolivian economic model and the presidency of Evo Morales depend to a great extent on the income derived from this hydrocarbon, being a fundamental factor for the future of the Plurinational Republic of Bolivia.

Brazil

Since 1999, Brazil has become the main destination for natural gas exports, being Bolivia's only client in the 2001-2005 period. This position allowed the entrance of Petrobras as the main investor in the sector until the year of the nationalization, which meant an important diplomatic friction between both countries. It was the complicity between Morales and Lula, as well as the importance of maintaining harmony between the leftist governments in the region, which allowed avoiding a major confrontation between the two countries. Despite the words of Petrobras' president in 2006, Sergio Gabrielli, announcing the end forever of the company in Bolivia, it has continued to be an important investor due to the profitability of its activities and the strategic importance of Bolivian gas for Brazil.

It seems clear that natural gas will play an important role in Brazil's future, since the main source source of electricity in the country, hydroelectric power, requires other sources to replace it when there is a shortage of rainfall, as occurred between 2012 and 2014. This context favored the entrance of natural gas in the electricity mix, which went from 5% in 2011 to 25% by 2015[10]. However, Brazil started a decade ago with the revolutionary pre-salt hydrocarbon exploitations, which have allowed the country to increase its crude oil production from 1.8 mbd in 2008 to 2.6 mbd in 2018. Natural gas production associated with these fields is expected to enter the Brazilian market as the necessary infrastructure connecting the off-shore fields to the still insufficient network of gas pipelines is built, something that is expected to improve with the entrance of private players to the sector following the 2016 energy reform. Likewise, Brazil already has 3 plants to import LNG, allowing it to diversify its imports, as it did during 2018 when Bolivia was unable to supply the 26 million cubic meters per day agreed in 1999. All this puts Petrobras and Bolsonaro, located in the ideological antipodes of Morales, in a privileged position for negotiation, and who could bet on increasing imports of the increasingly cheaper North American LNG and reducing the volume of Bolivian gas. In any case, due to certain non-compliances in the supply of gas from Bolivia, the contract will be extended for at least two more years until the pending volumes of submit , which Brazil has already paid for, are reached.

Argentina

The other natural gas market for Bolivia is also undergoing profound transformations, in this case derived from unconventional shale and tight oil techniques. The Vaca Muerta field, considered one of the largest shale deposits in the world, has begun to produce the first returns after years of investments by YPF and other multinationals. Despite Argentina's economic instability and the fiscal reforms demanded by the IMF that will delay the total development of this giant field[11], it is expected that by 2022 its production will cover approximately 80% of Bolivian imports, returning to the path of self-sufficiency achieved in much of the 1990s and 2000s[12]. For the time being, Argentina has already managed to renegotiate the volumes of natural gas imported in summer and winter in a way that is more favorable to domestic demand[13]. In addition, Argentina authorized natural gas exports to Chile after 12 years of interruption[14] and made its first LNG export in May 2019[15], which are early signs of growing domestic production.

It seems clear that the Argentine market will not have a long run for Bolivian natural gas and will probably put an end to its imports when the contract ends in 2026. Other options are to use the complete network of Argentine pipelines as transit to other destinations via LNG or to neighbors such as Uruguay, Paraguay or even Chile.

Peru

For some months now, Bolivia has been engaged in a public diplomacy campaign to extend a gas export pipeline to Puno, a Peruvian city located on Lake Titikaka. Although Peru has significant natural gas production in Camisea that allows it to export large quantities of LNG, the country launched a program known as Siete Regiones (Seven Regions) to universalize access to natural gas. Southern Peru can be supplied more economically through Bolivian imports due to the proximity of the La Paz pipeline, but there is reluctance, especially in the pro-Fujimori civil service examination , to import a surplus good in the country. This formula would be integrated into a plan to export liquefied petroleum gas from Bolivia to the same area, while Peru would build a gas pipeline to import oil and derivatives from the Pacific port of Ilo to La Paz. For Bolivia, the Peruvian market may be a temporary solution while exports continue to diversify, but it will have an early expiration date given the Peruvian natural gas reserves, double the Bolivian reserves, and the logical trend towards greater domestic production to cover the demand of the entire country. Likewise, it seems sensible to think that the Peruvian coast will in the future be one of the points through which Bolivia could export its natural gas in the form of LNG if the regional market is saturated.

Chile

From an economic point of view, Chile is the most attractive country for Bolivian exports. It lacks natural gas reserves and its mining area, with high energy demand, is located in an area relatively close to Bolivia's gas pipelines and fields network . However, the now century-old dispute over Bolivia's original territories annexed by Chile in the War of the Pacific (1879-1883) has been an insurmountable obstacle in the present century. It is worth mentioning that during the 50's and 60's Bolivia exported oil to Chile and the USA through the Sica Sica-Arica pipeline; that is to say, the refusal to export natural gas to Chile has been a flag used by Evo Morales and not a historical tradition in the relationship between these countries.

After the huge mobilizations caused by the Gas War, Evo Morales was able to catalyze popular fervor and use the territorial dispute to increase his popularity. In fact, a good part of his efforts in the previous legislature were focused on achieving the longed-for exit to the sea through the International Court of Justice in The Hague. In 2018 this court ruled favorably for Chile, ruling that this country has no duty to negotiate with Bolivia a territorial settlement. Morales' refusal to export natural gas to Chile looks set to continue for the duration of his presidency.

However, the 1904 Treaty of Peace and Friendship signed by both states grants Bolivia full customs autonomy in the Chilean ports of Arica and Antofagasta and the right to keep goods in transit for 12 months, with free storage for its imports, and 60 days of free storage for its exports. These conditions seem ideal for the construction of an LNG plant in Arica or Antofagasta to export natural gas by sea while supplying the Chilean north, in need of cheap natural gas to displace coal. The difficult political relations between both countries complicate the viability of this project, which should not be discarded when Morales leaves the presidency and there is greater harmony, as happened with Pinochet and Banzer in power.

Domestic consumption

Domestic consumption of natural gas in Bolivia has grown at an annual rate of 4.5% in the 2008-2018 period driven by subsidized prices for consumption and the implementation of state projects that aim to provide added value natural gas extraction such as the Bulo Bulo urea plant or the Mutun steel industry. It is expected that per capita income in Bolivia and electricity consumption will continue to increase over the next decade. If the volume of natural gas subsidies grows similarly while export revenues decline, Bolivia's delicate fiscal balance could take a similar path to that of Argentina. The process of domestic industrialization through natural gas does not seem far-fetched either, as long as it is based on market rules and not at the expense of public finances. The country has already achieved self-sufficiency in fertilizers and is already a growing exporter, an example of the economic diversification pursued by the Morales government.

The question: Is there a market for everyone?

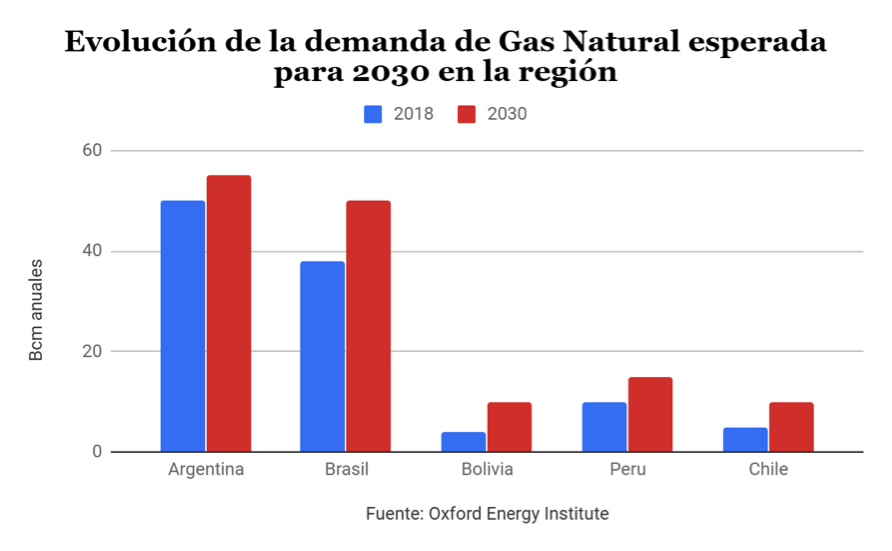

After reviewing the regional context, it may appear that the natural gas market in South America will be saturated by future oversupply. As can be seen in the graph, natural gas demand in the Bolivian neighborhood will increase from 107 bcm to 140 bcm per year by 2030. Peru, Argentina and Brazil are likely to increase their production and may reach self-sufficiency during the 2020s. This complicates the commercialization of Bolivian gas, but does not make it impossible. In the first place, the geographical reality of South America makes certain cross-border projects more economical than other internal ones, as in the case of southern Peru. Likewise, the increasingly lower costs of exporting gas by sea make it possible to find a market for surplus regional production, as in the case of Peru, which concentrates its gas exports to Spain. In a context of increasing energy interconnection, Bolivia will be able to continue exporting natural gas, albeit from a less privileged position and having to invest in export infrastructure. The major challenges are focused on increasing exploration activities by attracting more foreign and private investment, as well as the search for new markets, with the Chilean issue being a central element in this discussion.

[2] http://www.realinstitutoelcano.org/wps/portal/rielcano_en/content?WCM_GLOBAL_CONTEXT=/elcano/elcano_en/zones_en/ARI%20130-2006

[5] https://www.efe.com/efe/english/business/bolivia-to-spend-450-mn-in-2019-exploring-for-natural-gas/50000265-3881056

[6] https://www.ypfb.gob.bo/es/14-noticias/332-planta-de-amoniaco-y-urea-registra-avance-del-64.html

[7] https://www.petroleum-economist.com/articles/midstream-downstream/pipelines/2018/weighing-bolivias-gas-export-options

[9] https://www.petroleum-economist.com/articles/politics-economics/south-central-america/2017/bolivia-another-strike-from-the-resources-curse

[11] http://ieefa.org/wp-content/uploads/2019/03/Financial-Risks-Cloud-Development-of-Vaca-Muerta_March-2019.pdf

[13] https://www.reuters.com/article/us-argentina-energy-gas/argentina-renegotiates-key-gas-supply-contract-with-bolivia-idUSKCN1Q402O

The Belgian city, the world's capital of diamonds, has applied more regulations, sanctions and scrutiny on the industry, but still there are some bad practices

▲ The diamond industry has its main world center in the Belgian city of Antwerp

ANALYSIS / Jokin de Carlos Sola

The diamond trade moves hundreds of millions of euros every year around the globe. Most of them come from third world countries where the diamonds are extracted by very hard means. Even today, diamonds coming from conflict zones and used to finance conflicts and violence are a significant part of the market. Nowadays the production is mainly sold in cities of the United States and Europe and most of those diamonds in some way or another end up passing through the city of Antwerp in Belgium, showing that the Dutch and Belgians still have certain control over the industry.

This text will explore the origins of the city of Antwerp as a centre in the diamond market and of the control by Dutch and Belgians of this particular business; then it will analyze this industry in the new globalised era, and finally explain the relation of the city of Antwerp and the trade of blood diamonds.

Low Lands, a land of diamonds

Until the 19th century most diamonds came to Europe from India through the ports of Bruges, Antwerp and Amsterdam. The origins of the Low Countries as a centre of diamond craft and trade comes from the 15th century. In 1475 a Flemish jeweller, named Lodewyck van Bercken, invented the scaif, a polishing wheel infused with diamond dust and olive oil. This made easier the cutting of a diamond and revolutionised the industry. Bercken was a protégée of Duke Charles de Bold and his techniques were spread all around the Low Countries. For the next years Antwerp and Amsterdam became big competitors in the diamond trade.

In the 17th century Amsterdam was the most important city in Europe concerning diamonds. Because of the religious tolerance of the Netherlands, many Sephardic Jews established themselves in the city moving from Antwerp. There they had acquired knowledge working with diamond due to the guild-system, for the only industry that they were allowed to work in was the diamond industry.

In 1725 diamonds were discovered in Brazil and most of them went through Amsterdam. During the 19th century over 90% of rough diamonds sold in Europe passed through the Dutch city. Due to the colonial power of the Netherlands, the Dutch diamond trade extended over the world, especially to New Amsterdam (New York) and Cape Town, which would become vital instructions of the international diamond trade in the 20th and the 21st century. However, after the mines in Brazil started to dry up and the power of the Netherlands began to fade Amsterdam started to lose importance in favour of Antwerp, its biggest rival on the diamond industry, also a culturally Dutch city that would become the diamond's capital of the world. During its golden age Amsterdam developed a high-quality craft industry, but Antwerp managed to be as effective and cheaper as well as more permissive regarding taxes.

In 1866 diamonds were discovered in South Africa, in the Transvaal region, an area mainly populated by Dutch settlers. At the same time the British magnate Cecil Rhodes created the diamond company De Beers, based in Johannesburg. Massive amounts of rough diamonds started then to arrive to Europe, through Cape Town and Antwerp.

By the beginning of the 20th century De Beers controlled over 90% of the diamond industry in the world. In 1927 the company passed from the hands of Cecil Rhodes to the ones of Ernst Oppenheimer, a white South African entrepreneur, whose family still controls the diamond trade around the world.

During the Second World War most Jews from both Amsterdam and Antwerp were either forced to flee or were sent to extermination camps. This had hard consequences on an industry that was mainly controlled by the Jewish community. After the war, Antwerp quickly rebuilt its diamond business.

In 1948, De Beers established a new marketing strategy: it presented diamonds as a symbol of love and marriage, with the motto "a diamond is forever". A ring with a diamond became the perfect wedding present and it was advertised extensively. This new strategy increased the demand of diamonds, especially in the United States, where not just the economic elite was buying them, but it was also the aspiration of the high-middle class and even of the middle class. As a result, De Beers experienced it biggest growth in history turning Antwerp the indisputable capital of the diamond industry.

In 1973 the Antwerp Diamond World Centre (ADWC) was established. It is a public/private corporation, founded by the Belgian government and the most important diamond companies in the city. The Diamond Office, an ADWC's subsidiary, facilitates the import and export of diamonds in and out of Antwerp.

Antwerp's diamond industry

The Antwerp's diamond industry is concentrated in a part of the city called the diamond district or Diamantkwartier, which covers a complete square mile. According to the ADWC, 84% of the rough diamonds and 50% of the polished ones pass through Antwerp. In 2012 the turnover of the Diamantkwartier was 54 billion euros. Over 16 billion dollars in polished diamonds pass through the district's exchanges each year. There are 380 workshops that serve 1,500 companies. There are also 3,500 brokers, merchants and diamond cutters. The main actions taken in Antwerp are both the trade of rough and cut diamonds and the cut of rough diamonds with modern machinery. They also perform other jobs like applying color and crafting jewellery. There is even a bank consecrated to the diamond industry, the Antwerp Diamond Bank, which is owned by the KBC Bank.

Traditionally the Jewish community had almost complete control over the diamond business in Antwerp. More than 80% of Antwerp's Jewish population works in the diamond trade. In fact for many years the Yiddish was considered the main language of the diamond exchange. No business is conducted on Saturdays. However, since the late 20th century many Indian, Arminian and Lebanese dealers have increased importance in Antwerp's diamond trade.

For Belgium, the importance of Antwerp as the diamond capital of the world has been a source of economic incomes and great prestige. The diamond trade counts for 5% of Belgium's exports to the EU and 15% of its exports outside the EU; it is the 5th largest industry in the country. It also has been the reason for a lot of foreign investment.

During the last decade several other cities outside Western Europe have invested on their diamond industry, like Tel Aviv, Tokyo, Hong Kong, Chicago and several cities in South Africa. However, Antwerp still is the most important trade centre in Europe, being Amsterdam its biggest competitor.

In 2017 Antwerp traded 46 billion dollars in diamonds, with a total of 233.6 million of carats. This figures meant a slight improvement, aided by the approval of the Diamond Regime by the Belgian Parliament. This law changed the way of taxation and ended up benefiting the diamond companies of Belgium.

Diamonds and political corruption

Because of its size and the profits it generates, the diamond industry has a lot of influence in Belgian politics, especially in Flanders. It acts as a lobby in favor of specific bills and policies and tries to avoid an increase of regulations. An example of this is when in 1986 an investigation was opened on the business of Abraham Kirschen, who reportedly sold diamonds in the black market to avoid taxation. According to the average, some conservative politicians were linked to the scheme and some 170 diamond traders were investigated for evading a billion dollars in taxes through a bank account in Geneva. The case ended up implicating the second largest diamond company after De Beers, Omega Diamond, and most of the Belgian political establishment. The AWDC rapidly distanced itself from the scandal at the beginning of the controversy, which was to closed without having much negative impact in the industry.

Following this and other scandals, the Belgian government managed to impose more regulations, in order to rule a business that traditionally has shown a lack of transparency and has been prone to tax evasion. But the diamond lobby has been very active and through its political influence has scored some victories. In 2011 it achieved its main goal: the change of the Belgian criminal law.

In 2008 the biggest fraud of a diamond company was discovered by Belgian authorities. The company was Omega Diamonds, established only in 1994 by the Belgian Sylvian Goldberg. The company became the second biggest diamond company after De Beers and had for many years the monopoly of the diamond exports from Angola. An investigation started in 2006 concluded that the company had created a tax fraud scheme. Omega Diamonds imported diamonds from Angola and the Democratic Republic of Congo through Dubai into Antwerp. During the transfer, documents were manipulated allowing the company to conceal the origin of the diamonds. It ordered the shipment of diamonds purchased in Angola and the DRC to be delivered to entities located in Dubai. Upon arrival in Dubai the diamonds were repacked and exported to Antwerp. The new shipment, marked "diamonds of mixed origin", was issued with an invoice addressed to Omega Diamonds wherein the value of the diamonds was artificially increased. In so doing, the company was able to hide its additional profit from Belgian tax authorities.

In October 2008, Belgian federal police raided the premises of Antwerp-based Omega Diamonds. The raids resulted in a record seizure of 150 million dollars worth diamonds. Companies in Antwerp started to fear similar scrutiny from Belgian courts and the federal police. Because of this, the AWDC asked for political support, and it got help from some politicians, who accused law enforcement of "damaging the reputation" of the diamond industry. A bill meant to block law enforcement from confiscating illegal diamonds, written by AWDC's lawyers, was introduced by members of the most important political parties of the Belgian establishment.

In December 2010, the sponsors of the 2008 bill became members of a secretive group, "The Diamond Club", in order to push this legislation, which passed in 2011. According to the law, diamond companies investigated by fraud could avoid prison by paying a sum of money to the public prosecutor, as well as fight back the judicial backlog, and prevent, in many cases, a deeper investigation.

In application of the law, Omega Diamonds agreed in 2013 to pay a settlement of 160 million euros to avoid being prosecuted for tax evasion and money laundering, all that for a fraud that is calculated to have been of over 2 billion euros. The settlement cleared Omega Diamonds of all charges.

The law was controversial, to say the least, and it became very unpopular in Belgium, mainly because almost all parties were involved in it. In 2016 the Federal Constitutional Court of Belgium declared unconstitutional most parts of it. In 2017, the Belgian Parliament set up an inquiry commission to investigate the relation between the law of 2011 and the diamond industry. The commission stated that the blueprint of the law was written by lawyers for the AWDC, but at the moment it hasn't investigated the relations of various politicians with the diamond industry.

Blood diamonds

A blood diamond is the one that is extracted from conflict zones and used for financing wars or violent actions. They have been a very common threat to the image of the diamond industry and nowadays there is a big effort by various diamond companies of tracking the origin of the stones, in order to avoid scandals. However, during the 1980s and 1990s blood diamonds worth millions of dollars flooded from Angola and Sierra Leone to Antwerp, something that still happens today.

Diamonds have a very big value, that's common knowledge, but in fact a big reason for this value comes from a strategy started by De Beers and followed by other diamond companies. This strategy consists of acquiring the monopoly of diamonds in a certain region and putting them in the market in a way that prices will always remain high. This was firstly done by Cecil Rhodes, and the diamonds in South Africa. If all the diamonds were put in the market at the same time their price will decrease. With this the company always got a big revenue.

Before the Angolan Civil War (1975-2002) there was not much concern on what was the origin of the stones. However, during this war the UNITA group started to use the diamonds extracted in their territory to fund its war against the government. This made diamonds a reason for instability and provided violent groups with weaponry. Because of this there was a big international pressure for the ending of the trading of the Angolan diamonds in 1998, by the UN Security Council resolution 1173.

A similar situation happened in Sierra Leone with RUF group and its war against government (1991-2002). It is calculated that the RUF extracted yearly a total of 125 million dollars every year. This money was used to fund a war were the RUF committed a series of crimes such as rape, mass killings or mutilations. In the year 2000 the UN Security Council imposed sanctions on diamonds from Sierra Leone.

Even though these sanctions were harmful for both rebel movements a report written by Robert Fowler, chairman of the Security Council committee investigating violations of sanctions on Angola, informed the UN that blood diamonds were still being exported from these countries, most of them arriving to Antwerp, where they were sold in the international market.

|

The 2017 African Diamond Conference organized by the Antwerp Diamond World Centre [ADWC]. |

![The 2017 African Diamond Conference organized by the Antwerp Diamond World Centre [ADWC].](/documents/10174/16849987/diamonds-blog-2.jpg "The 2017 African Diamond Conference organized by the Antwerp Diamond World Centre [ADWC].")

The Fowler Report

The Fowler report was very critical with the role of Antwerp as the end stage of all blood diamonds. "The unwillingness or inability of the diamond industry, particularly in Antwerp, to police its own ranks is a matter of special concern to the panel,'" said the report.

The report also stated that the willingness to traffic the diamonds provided by UNITA or RUF "results from the often-expressed fear that stricter regulation would simply cause traders to take their business elsewhere." It also said that he Belgian authorities had failed to establish a credible system for identifying rough diamonds coming from conflict zones, while making "no serious effort" to keep track of diamond traders known to deal with the rebels. A prominent Antwerp diamond trader trained the diamond experts who work for UNITA, the report said.

The system for concealing the bad practices consisted on transporting the diamonds to third countries that were willing to act as a bridge between the diamond exporter and Antwerp. Two examples of this are Liberia for the Sierra Leone diamonds and Rwanda for the stones from Angola. In fact, Rwanda had a key role in the war in Angola: UNITA transported diamonds to Rwanda which were bought by Antwerp diamond traders and then the money was used to buy guns from Eastern Europe that were transported to Rwanda.

The Fowler report, together with another investigation made by the international NGO Global Witness, also pointed De Beers to have bought Angolan blood diamonds to maintain its monopoly on diamond sells. De Beers admitted to have done this before the sanctions of the UN, but Global Witness still accuse De Beers of trading with blood diamonds even after the sanctions. According to this report the company bought blood diamonds through its huge network of buying offices in Africa and the company's cartel-like Central Selling Organization, which sets world diamond prices (although it is based in London, many of its diamond traders work in Antwerp).

This severely harmed De Beers' name. Because of this Anthony Oppenheimer, CEO of the company, stopped buying Angolan diamonds except the ones provided directly by the Angolan government. Due to the fall of prestige of diamond industry after the scandals involving blood diamonds De Beers and other diamond companies started to establish more transparent roots of diamond trading to avoid new scandals.

The Kimberly Process

After the effects of the Fowler report the Kimberly Process of Certification Scheme was established to guarantee a fair and clean trade of diamonds. Established in 2003 following a meeting in Kimberly, South Africa, and by the UN General Assembly Resolution 55/56. Belgium took an active role in the establishment of the process. The first step of these process was the system of warranties created by World Diamond Council, all these warranties were incorporated in the Kimberly Process and all its members must follow them:

-Trade only with companies that include warranty declarations on their invoices.

-Not buy diamonds from suspect sources or unknown suppliers, or which originate in countries that have not implemented the Kimberley Process Certification Scheme.

-Not buy diamonds from any sources that, after a legally binding due process system, have been found to have violated government regulations restricting the trade in conflict diamonds.

-Not buy diamonds in or from any region that is subject to an advisory by a governmental authority indicating that conflict diamonds are emanating from or available for sale in such region, unless diamonds have been exported from such region in compliance with the Kimberley Process Certification Scheme.

-Not knowingly buy or sell or assist others to buy or sell conflict diamonds.

-Ensure that all company employees that buy or sell diamonds within the diamond trade are well informed regarding trade resolutions and government regulations restricting the trade in conflict diamonds.

Members like the Democratic Republic of Congo have been expelled after being unable to ensure the origins of the stones. Organizations such as Global Witness have criticized the ineffectiveness of the process and its inability to end with the continuing trade of blood diamonds: "Rough and uncut diamonds can easily be smuggled over porous borders from places like the Ivory Coast and can obtain a Kimberley Process certificate from another country before being shipped to Europe". Other critics accuse the Kimberly process of making the diamond trade too complicated and too bureaucratized and therefore harming developing countries which heavily depend on the diamond trade such as Botswana or South Africa. They underscore that only 0.2% of diamonds in the industry are considered conflict diamonds and during both Angola and Sierra Leone civil war the number never increased over 15%, as it was addressed by the publication Foreign Policy.

The Belgian connection

Despite the efforts of the Kimberly Process and the Belgian government blood diamond still pass through Antwerp, mainly using companies and bank accounts in Switzerland. An example of this was when in March of 2017 Belgian authorities seized 14 million euros worth of diamonds believed to be from the Ivory Coast from a major diamond smuggling ring based in Antwerp. The investigation also led to several Geneva-based firms that used fake certificates to import raw diamonds worth 370 million euros from countries outside the Kimberley Process before selling them to Belgian traders.

Antwerp dealers routinely settle multi-million-dollar transactions in cash and rarely offer receipts, according to a study on diamonds and conflict in Sierra Leone by the NGO Partnership Africa Canada. While illegal operations have a hand in keeping the trade alive in Europe, even legitimate enterprises could be unwittingly involved.

Another case was when in 2015 the Belgian businessman Michael Desaedeleer was arrested in Spain, accused of enslavement and pillaging blood diamonds during Sierra Leone's civil war. His arrest was a "landmark" because it was the first time an individual resulted detained on international charges related to the exploitation of the war in Sierra Leone to market blood diamonds.

Recently, Zimbabwe has gained recognition as an exporter of blood diamonds and a 2017 report by Global Witness relates these diamonds with the Antwerp diamond industry. Like most of its neighbours, Zimbabwe has diamond mines in its territory. However, in 2006 in the area of Marenga the richest diamond deposits were found -the so called Marenga diamond field. Since its discovery, the extraction of these diamonds has been done either by the government or by companies related to the regime. According to Global Witness these stones are being used to strength the regime and keep the political repression. Because of that most countries and organizations consider it blood diamonds. Since its discovery, there has been an embargo of these diamonds, but the Antwerp industry has tried to make the trade flow between Zimbabwe and the city, sometimes violating the EU sanctions.

The report mentions confidential government papers that talk about deals between Belgian diamond traders with the Zimbabwean Consolidation Diamond Company (ZCDC), as well as with two other companies in Marenga: Anjin and Jinan, both related to the state-owned military company Zimbabwean Defence Industries (ZDI). Since 2008, the EU imposed sanctions on ZCDC as well as on Anjin and Jinan. However, in 2013 the EU decided to withdraw all sanctions against ZMDC following increasing pressure from state members, especially from Belgium (pressed by the AWDC). The decision was very criticised by human rights groups, and finally the sanctions against the ZDI were kept.

Since 2010 Zimbabwe has officially exported over 2.5 billion dollars in diamonds according to official figures from the Kimberley Process. According to the limited available government reporting, only around 300 million dollars can be clearly identified in public accounts.

The diamond trade is definitely part of the Belgian trade tradition and part of the Belgian economy. As a part of a country with very few natural resources, Antwerp has done around history a big effort to maintain its position as a diamond centre. Bringing money, jobs and prestige to the city. However, it has also brought corruption to the political system and has served as a place for money laundry, tax evasion and financing of violent groups in Africa. With corruption, with money, with prestige and by work and schemes, without question Antwerp is the diamond of Belgian crown.

The meeting COP24 made progress on regulating the Paris agreement , but "carbon markets" remained blocked.

Mobilisations for governments to take more drastic action on climate change can make us forget that many countries are taking real steps to reduce greenhouse gases. Although international summits often fall short of expectations, climate agreements are gradually making headway. Here are the results of the last such summit: a small step, admittedly, but a step forward.

![Plenary session of COP24, held in December in Katowice, Poland [COP24].](/documents/10174/16849987/cumbre-clima-blog.jpg "Plenary session of COP24, held in December in Katowice, Poland [COP24].")

Plenary session of COP24, held in December in Katowice (Poland) [COP24].

article / Sandra Redondo

The climate summit (also known as COP: Conference of the Parties) is a global lecture prepared by the United Nations, where measures and actions related to climate policy are negotiated. The last one, dubbed COP24, took place from 2 to 14 December 2018, in the Polish city of Katowice. It was attended by around 3,000 delegates from 197 countries that are party to the United Nations Convention on Climate Change framework . Among them were politicians, representatives of non-governmental organisations, members of the academic community and the business sector.

The first COP took place in 1995, and since then these summits have led to the creation of the Kyotoprotocol (COP3, 1997) and the Parisagreement (COP21, 2015), among other mechanisms for international action. The main goal of the quotation in Katowice was to find a way to implement the 2015 Paris agreement , i.e. to implement cuts in pollutant emissions to avoid an increase in global warming. COP24 was the last summit before 2020, when the Paris agreement will enter into force.

goal The 2015 Paris Agreement agreement was signed by 194 countries with the aim of preventing pollutant emissions, which cause the greenhouse effect, from increasing the planet's temperature above two degrees Celsius Degrees compared to pre-industrial levels. Degrees The international community is calling for a concerted effort to ensure that the temperature increase does not exceed 1.5°C above pre-industrial levels. The summit aimed to create a clear, concrete and common outline to be followed by all countries in order to make agreement a reality.

Challenges

One of the challenges in achieving this goal lies in establishing a balance that allows all nations to participate in this struggle, but taking into account the reality of each one of them: the different technological and financial capacities, as well as the circumstances of vulnerability and historical contamination. As countries with great differences among them are involved, the task of reaching consensus is understandably difficult. This was one of the measures intended to be implemented from the Paris agreement , in which governments pledged to help countries at development to achieve greater and more permanent adaptation.

In the words of Patricia Espinosa, UN Climate Change Executive administrative assistant , in addition to measures to make the Paris agreement effective, it is important to "promote a cultural change in the ways our societies produce and consume in order to rethink our models of development".

Wang Yi, China's foreign minister, said that his country reaffirms that only a joint work among all countries will provide an effective solution in the fight against climate change.

At these summits, agreements must be accepted by all participating states, which can cause negotiations to drag on. This is what happened at COP24. Negotiations were scheduled to end on Friday, but dragged on until the final agreement was reached the following day. The final text, C by all countries in attendance, turned out to be less ambitious than expected, especially on reference letter on greenhouse gas emission cuts.

Despite the declarations of willingness of some countries, certain tensions were inevitable in the negotiations, especially when it came to the assumption that more ambition is needed in this fight. On the one side was the conservative side, with countries such as the United States (which is one of the countries that contributes the most CO2 per capita to global warming) and Saudi Arabia among others. On the other side were the European Union and other states, some of them island states, threatened by rising sea levels, which will continue to rise as a result of rising global temperatures.

Another cause of delay was a demand from Turkey at the last minute to improve financing conditions. With regard to financing, the final agreement acknowledges that more resources need to be devoted to this fight, particularly to the reduction of greenhouse gases.

report of the International Panel on Change

In addition to the measures and cuts that were agreed at this summit, a declaration was to be made with the conclusions of the experts'report group Intergovernmental Panel on Climate Change (IPCC), which would warn that the world does not have much time left to avoid the worst consequences of climate change.

This report, which was one of the big battles of the summit, details what will happen if the global temperature rises 1.5 Degrees centigrade above pre-industrial levels. Currently the temperature is one Degree above pre-industrial levels. Despite the fact that it should have been considered of great importance by all countries, given that these are facts that affect the world, there were countries such as Russia, Kuwait, the United States and Saudi Arabia, which tried to play down its importance and raised doubts about the veracity of the conclusions of the report, while other states defended the unquestionability of the conclusions. A common characteristic of these opposing countries is that they are the world's major oil producers.

The report of the International Panel on Climate Change (IPCC), presented at COP24, indicates that, if no change continues, between 2030 and 2050, these will be the consequences:

-Increase in flood risk from 100% (at 1.5°C) to 170% (at 2°C).

-If we exceed 1.5°C, more than 400 million people living in cities will be exposed to extreme droughts by the end of the century.

Arctic ice will decrease so much that there will be an ice-free summer at least once every 10 years.

-150 million deaths could be avoided by limiting this 1.5°C temperature rise.

-Nearly 50 million people could be affected by a sea level rise by 2100 if the temperature increase exceeds 1.5°C.

-Corals would be among the worst affected, as they would all be lost by 2100 if the 1.5°C rise is exceeded due to rising ocean acidity. Reaching 1.5°C would result in the loss of 70% of them.

According to calculations also made by the IPCC, CO2 emissions will have to fall by 45% by 2030 to limit warming to 1.5 Degrees. In addition, "carbon neutrality" must be achieved by 2050, i.e. to start having negative emissions, i.e. to stop emitting more CO2 than is removed from the atmosphere. The longer it takes to implement these measures, the less time we will have before the negative consequences affect us all, and may even become irreversible. With each passing year, not only are greenhouse gas emissions not being reduced, but they are increasing. That is why now is the time to act.

As a conclusion of the IPCC's report it should be clear that in order to avoid an increase above 1.5 Degrees it was necessary to cut current emissions by 45%. However, due to the disagreement of several states with this report, and the fear of the failure of the summit, these cuts were omitted from the final agreement . This delay in taking drastic action only reduces the time we have to save our planet, risking being too late to avoid the worst consequences.

result

At meeting in Katowice it was possible to reach consensus on the regulation of the Paris measures agreement , which is already a great achievement, but the agreement came at the cost of setting aside carbon markets, i.e. the set of carbon trading mechanisms that allow countries that emit more greenhouse gases to buy emission rights from those countries that do comply with the targets and emit gases below the established limit. This section blocked the negotiation of other issues for hours, as several countries that benefit from the current status, such as Brazil, opposed modifications. Finally, it was decided to postpone the negotiations until the COP25 meeting next year in Chile.

The common set of rules for all countries allows them to present their progress in the fight against climate change in the same way. We have to remember that the problem after agreement in Paris was that each country decided to present the data pledge cuts in a different way. For this reason, a agreement to unify rules and criteria in a common way is a breakthrough. These transparency rules are particularly important, as they will make it possible to analyse the progress of what has been proposed at each point in time, and this will make it possible to analyse the targets achieved and the need for further action. For example, among the data that all countries are required to include in their reports are the sectors included in their targets, gas emissions and the year of reference letter against which they will measure the process.

Although some are disappointed that they expected more results than were achieved, the mere fact that agreement was reached among all the participating countries must be considered a success.

We must bear in mind that some of the participating states that showed less interest and put less effort into the negotiations for this fight, and even raised obstacles in the negotiations, are very important countries in the international sphere, with great economic and political power. For this reason, we should consider the agreement reached as a further step towards raising awareness of the fight against climate change. A small step, but a step forward.

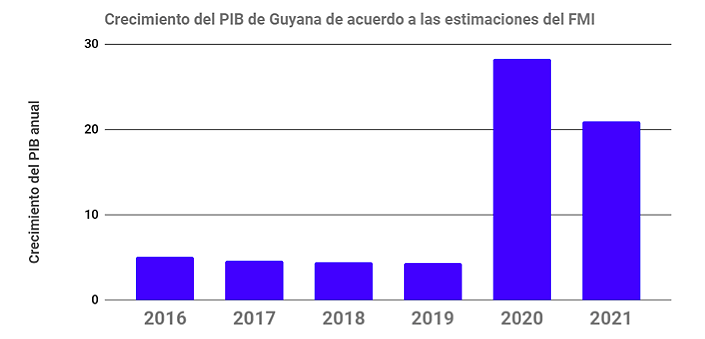

One of the poorest countries in the Americas may become the world's largest oil producer per capita, disrupting the relationship with its neighbors.

Promising oil discoveries in Guyana's waters augur greater regional relevance for this small and poor South American country. Territorial disputes between Venezuela and its neighbor, on account of the Essequivo territory that Caracas has historically claimed (more than half of Guyana's surface area), may be exacerbated by the opening of wells in deep waters that Guyana administers but over which Venezuela seeks fair international arbitration.

Image created by ExxonMobil about its exploration in Guyana's waters.

article / Ignacio Urbasos Arbeloa

Guyana has found oil deposits 193 km off its coast by the hand of ExxonMobil that can completely change the course of its Economics and its international influence. After several decades of failed attempts in the search for hydrocarbons in its subsoil and an exhaustive search since 1999, in 2015 the Liza field responded positively to seismic analysis showing subsequently abundant oil reserves at a depth of 1,900 meters offshore. At the moment estimates speak of 3.2 billion barrels of recoverable oil to be found in the Guiana Basin, which extends to Suriname, another country with a promising oil future. Companies such as Total, Repsol or Anadarko have already obtained exploration rights in the different blocks offered so far by the Guyanese government, however it is the Stabroek Block, exploited by Exxon (45%), Hess (30%) and the Chinese CNOOC (25%), which will be the first to start producing, in 2020.

Expected to reach 700,000 barrels per day by 2025, this is the largest finding of the lustrum in deepwater globally and one of the most valuable additions to conventional oil production. The crude is Pass for middle distillates, precisely what Gulf of Mexico refiners are looking for in a market saturated by light crude from fracking. If agreement is to optimistic estimates, by 2025 this impoverished country of about 700,000 people would surpass OPEC member Ecuador in oil production, making it the world's largest producer of barrels per capita (ahead of current leader Kuwait, which has a production of 3.15 million barrels per day and 4.1 million inhabitants). Production costs per barrel are estimated at $26 considering taxes, so profits are expected to be abundant in practically any future scenario (currently the barrel of WTI is around $50), making Guyana one of the great attractions in the oil industry at the moment. Prospecting led by Exxon, a company that already dominates exploitation in the so-called deepwaters, had in 2018 fees hit rates close to 80%, which has generated enormous expectation in a sector accustomed to fees of 25%.

The positive impact that this finding will have for the Guyanese Economics is evident, although it is not Exempt of challenges, given the high levels of corruption or a bureaucracy and political class inexperienced for negotiations at this level. The IMF, which is advising Guyana, has already recommended freezing further negotiations until the tax system is reformed and the country's bureaucratic capacity is improved. The same agency has estimated a 28% GDP growth for Guyana by 2020, a historic figure for a Economics whose exports are based on rice, sugar cane and gold. The government is already designing an institutional framework to manage oil tax revenues and cushion their impact on other sectors. Among the proposals is the creation of a sovereign wealth fund similar to those of Norway, Qatar or the United Arab Emirates, which could become effective this year with partnership of experts from the Commonwealth, to which the country belongs.

Historic dispute with Venezuela

These new discoveries, however, increase the tension with Venezuela, which maintains a territorial dispute over 70% of the Guyanese territory, the Guayana Esequiba belonging to the Captaincy General of Venezuela during the Spanish Empire. The disputed territory was later de facto colonized by the British Empire when the British took control over the Dutch territories of Guyana in 1814. In 1899 an international tribunal ruled unanimously in favor of the United Kingdom against Venezuelan claims. However, later revelations demonstrated the existence of serious elements of corruption in the judicial process, making the award "null and void" (non-existent) in 1962. In 1966 the United Kingdom, as representative of British Guyana, and Venezuela signed the Genevaagreement , which established the commitment to reach an agreement agreement: the Port of Spain protocol of 1970, which froze negotiations for 12 years. After the end of this period, Venezuela demanded Guyana to return to direct negotiations, and in accordance with the United Nations Charter, the diplomatic formula of good offices has been agreed upon and remains in force to this day, without any significant progress having been made. Since Guyana's independence in 1966, Venezuela promoted an indigenous separatist movement in the region, Rupununi, which was harshly repressed by Georgetown, setting a precedent of military tension on the border.

Although a formal agreement has never been reached on the territorial dispute, the arrival of the socialist People's Progressive Party (PPP) to government in Guyana in 1992 and the electoral victory of Hugo Chávez in 1999 in Venezuela ideologically aligned both countries, which allowed them to reach Degrees of unprecedented cooperation during the first decade of the 21st century. In the framework of this golden era, Guyana participated between 2007 and 2015 in the Venezuelan Petrocaribe initiative, receiving some 25,000 barrels per day of oil and derivatives, which constituted 50% of its consumption, in exchange for rice valued on market price. On the other hand, Guyana supported Venezuela's candidacy to the United Nations Security committee in 2006 in exchange for an express promise by Caracas not to use the privileged position it temporarily acquired in the territorial dispute. An important precedent was the declaration of Hugo Chávez in 2004 of not opposing Guyana "to unilaterally grant concessions and contracts to multinational companies, as long as this favors the development of the region". In spite of the existence of unfriendly acts between the two States during this period, the vital importance that the Venezuelan anti-imperialist foreign policy gave to the Caribbean during Chávez's mandate, obliged him to treat topic from the most absolute moderation to avoid a disagreement with CARICOM and to maintain Guyana's support in the OAS.

|

Map of Guyana's oil exploitation blocks (in yellow), with the delimitation of territorial waters and Venezuela's claims. |

, with the delimitation of territorial waters and Venezuela's claims.")

New tensions

As a result of the oil discoveries, the historic territorial dispute with Venezuela has returned to the forefront. A change of sign in the Georgetown government has also contributed to this. The 2015 elections brought to power in Guyana the A Partnership for National Unity, led by former military officer David Granger. This is a multi-ethnic coalition that could be described as center-right and with less ideological sympathies towards neighboring Venezuela than those professed by the previous president, Bharrat Jagdeo of the PPP. At the end of 2018 there was an escalation of tension, following the seizure on December 23 by the Bolivarian National Navy of two Guyanese-flagged vessels belonging to ExxonMobil that were prospecting in the area and which, of agreement to the version of the Government of Nicolás Maduro, had entered Venezuelan waters. The international response was not long in coming and the United States urged Venezuela to "respect international law and the sovereignty of its neighbors". Precisely one of the most complex issues in the territorial dispute is the projection of the waters of each country. The position defended by Venezuela is to draw the maritime limits of agreement to the projection of the delta of the Orinoco River, as opposed to the Guyanese position which draws the line in a manner favorable to its territorial interests. Although this was a secondary element in the territorial dispute, the economic potential of these waters places them at the center of the discussion.

To all this is added the declaration of the group of Lima, of which Guyana is part, not to recognize the May elections in Venezuela and to threaten to economically sanction the country (although, to date, it has not recognized the opposition candidate Juan Guaidó as interim president). The international ostracism of the Bolivarian Republic has allowed Guyana to obtain important diplomatic support from the aforementioned group of Lima, CARICOM and the United States in relation to its international dispute and the detention of the Exxon ships.

result The future of relations between Venezuela and Guyana depends to some extent on the outcome of the future elections in March in the latter country, which will pit the hitherto president, David Granger, recently ousted from power by means of a motion of censure, against the leader of the PPP, Bharrat Jagdeo, whose party has maintained the best relations with Chavista Venezuela. The no-confidence motion is a historic milestone for the South American country, which will have to prove its social cohesion and political stability amidst geopolitical tensions and an international investment community that is watching closely the development of events.

|

|

Increased defense revenues

Georgetown, for the moment, limits itself to diplomatic action to defend its territorial sovereignty, but documents of the Guyanese Defense Forces prior to the oil discoveries already identified the need to develop military capabilities in case such resources were found in the country. According to Exxon's estimates, agreement , Guyana would earn 16 billion dollars a year from 2020, which would increase the military expense , currently at around 1% of the GDP. The Army of the Cooperative Republic of Guyana conducted in August 2018 the largest military exercises in its history, mobilizing 1,500 troops out of an Army estimated at around 7,000. Information available about the material resources of navy and aviation show the need for quantitative and qualitative improvement. Overcoming the existing ethnic divisions between the population of Indian and African origin must be one of the priorities of the Armed Forces, which suffer from a clear under-representation of the Indian community, a cause of historical suspicion of the civil society.

At final, the Caribbean region of South America will be marked in the coming years by the economic potential of Guyana and its struggle for territorial survival in the face of Venezuela's legitimate demands. Achieving a real development of the oil industry will undoubtedly be the best armor for its future as a sovereign and independent country. The political uncertainty in Venezuela, immersed in an enormous crisis, generates the fear of a possible military escalation as an escape valve to the internal economic and political pressure against a rival that lacks the resources to face it. The capacity of Guyana's political class to manage the brutal increase in its economic resources after 2020 is still an unknown, but it is possible to imagine that the second poorest country in the Western Hemisphere will reach great heights of development if it is capable of learning from its neighbors and managing a regional context that is favorable to its national interests.

Geopolitical misgivings about perceived foreign interests should not distract beneficiary countries from implementing sustainable use.

The Guarani Aquifer has given rise to a more political than scientific literature in South America, denouncing the alleged interest of great powers (formerly the United States, now China) to take away the water that naturally belongs to the countries of the region. These crusades often distract from a more indisputable fact: the risk comes not so much from outside as from uncontrolled practices and the lack of clear legislation in the aquifer countries themselves. This article reviews the results of some recent programs of study on the characteristics and status of the Guarani Aquifer.

▲ source: UC Irvine/NASA/JPL-Caltech

article / Albert Vidal

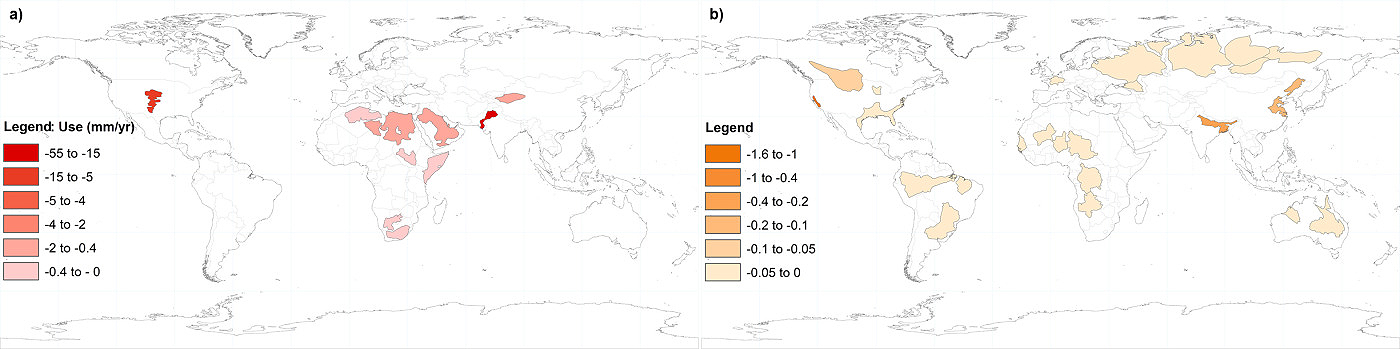

About one third of the large groundwater aquifers are at a critical status . Current technology does not allow us to accurately predict how much water we have left on the planet, and precisely because of this uncertainty, accelerated groundwater extraction is too great a risk not worth taking.

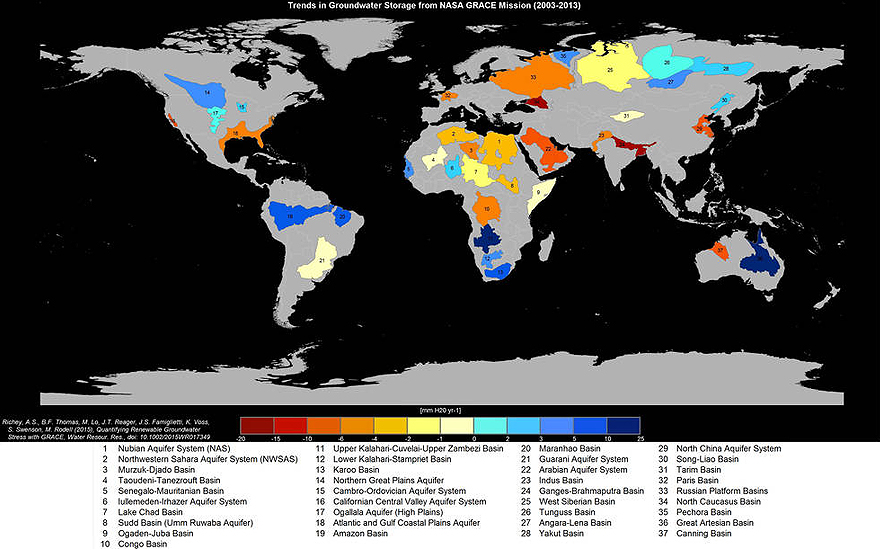

The map above shows the 37 largest aquifers in the world, which have been studied by a NASA satellitemission statement known as the Gravity Recovery and Climate Experiment (GRACE). This mission statement has attempted to measure the water levels in the aquifers, in order to check the water stress to which they are subjected, as well as their level of renewal. Of these, there are 21 whose extraction is not sustainable, and they are losing water very rapidly. Among these, there are 13 whose status is particularly critical (darkest red), and threatens regional water security. There are 16 other aquifers that enjoy sufficient recharge to not lose water or even gain water; these are marked in blue.

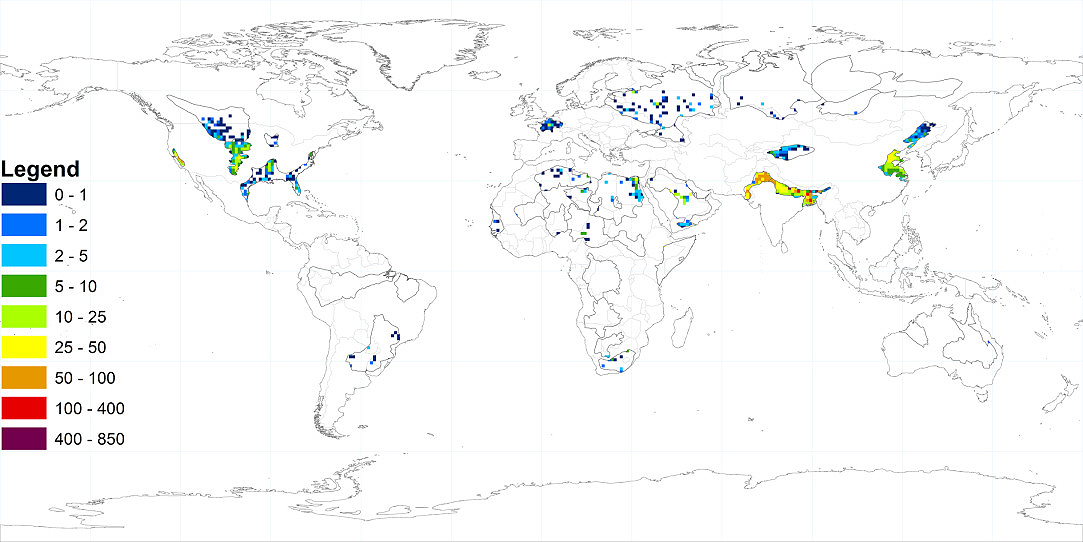

This NASA research , the results of which are analyzed in a study by Water Resources Research, divides aquifer water stress into 4 different types, from highest to lowest intensity: extreme stress, variable stress, human-dominated variable stress, and no stress. Let us now look at another map, collected in that study, which shows sample the spatial distribution of groundwater abstraction in the world:

|

source: Water Resouces Research |

The color of the dots indicates the intensity of extraction, measured in millimeters per year. Thus, this statistic sample is the sum of withdrawals for industrial, agricultural and domestic use. At first glance, it can be seen that the countries that suffer the most accelerated extraction are India, Pakistan, China, Egypt and the United States. In the case of the Guarani Aquifer, the extraction points are located in Paraguayan territory and near Sao Paulo, with an extraction of between 0 and 5 millimeters per year.

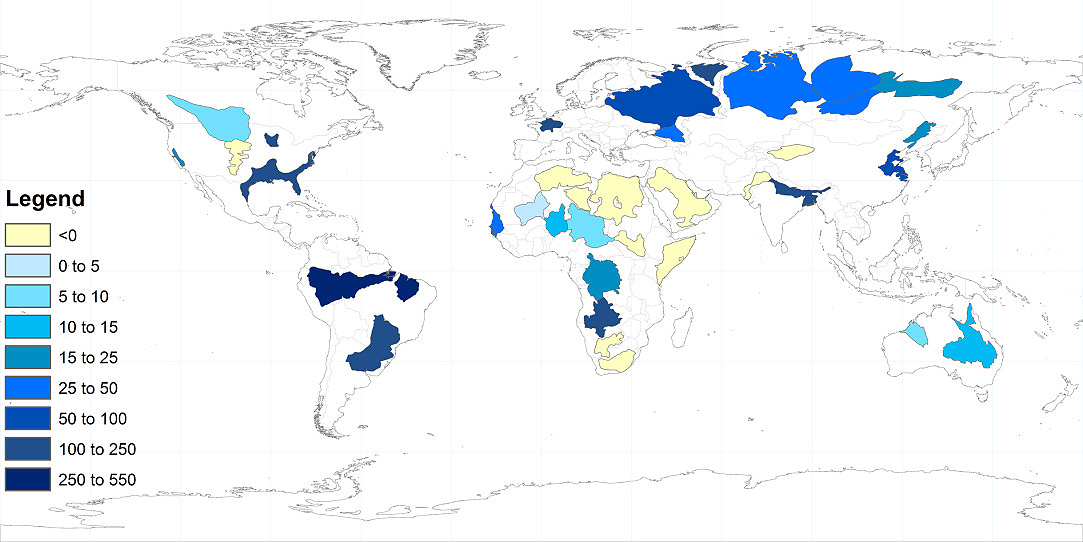

The research has produced other maps that may be useful to financial aid for a deeper understanding of the problem. In this case, the following map sample shows an average of the annual recharge of aquifers in the world.

|

source: Water Resouces Research |

The yellow color represents negative recharge, i.e., systems that are losing water. The blue color, on the other hand, marks those aquifers that have a positive recharge (the more intense the blue color, the greater the recharge). The Guaraní aquifer, in particular, has a recharge of 225 millimeters per year.

Finally, we will see two maps referring to the water stress of aquifers.

|

source: Water Resouces Research |

The countries listed above (a) suffer from extreme water stress, i.e., natural recharge is negative, and there is also intense human use. This particularly affects the African continent, the United States, the Middle East and the heart of Asia.

Here we show (b) those aquifers with a variable stress level. This means that they have a positive natural recharge, but at the same time there is a human use that could be detrimental. The Guarani Aquifer is included in the latter group.

The Guarani Aquifer

Making reference letter to a famous phrase from one of Franklin D. Roosevelt's speech - "with great power comes great responsibility"- we can say that the countries that enjoy access to the Guarani Aquifer System (GAS), must assume the responsibility that comes with having been endowed with this important natural resource . They know that, many times, such riches bring competition, unrest and even problems such as internal instability and tensions between some large companies and governments.

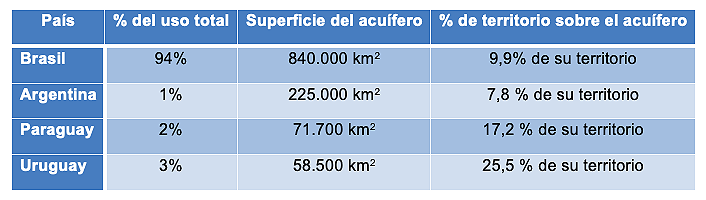

The SAG is a transboundary aquifer that extends below the surface across 1.2 million km2 between Brazil, Uruguay, Paraguay and Argentina. According to the most recent research, this is the third largest groundwater reservation in the world in terms of surface area, and contains about 45,000 km3. The low recharge capacity is the most common problem in the aquifers of our planet, since it is usually not enough to cover the amount extracted, thus jeopardizing their sustainable use. This system is particularly important because of its very high renewal capacity (between 160 and 250 km3 per year), which takes place thanks to the abundant rainfall that feeds it.

Challenges posed by