December 10, 2024

Published in

El Confidencial

Germán López Espinosa

Professor of the School of Economics

The General Situation in France

Michel Barnier, France's Prime Minister until Wednesday, December 4th, was ousted by a vote of no confidence backed by both the left and the far-right. This marks the second political crisis in France within six months. The political uncertainty arises at a delicate moment for the country, and the prospect of prolonged gridlock could worsen investor and creditor perceptions of the French economy.

In 2023, France recorded a fiscal deficit of 5.50% of GDP. The European Commission projects this deficit to rise to 6.2% in 2024, with unemployment expected at 7.4%. GDP growth is forecasted to improve to 1.1%, still trailing inflation, which is estimated at 2.4%.

The uncertainty has also impacted French sovereign debt. The yield on France's 10-year bond currently stands at 2.88%, higher than Spain's (2.73%) and significantly above Germany's (2.12%). France's 5-year Credit Default Swap (CDS)-a financial instrument providing protection against bond default risk-stands at 36.95 basis points. This means the annual premium is 0.3695% of the insured notional value, which is not alarmingly high. For comparison, Spain's CDS is 33.78 basis points, and Germany's is 12.51.

Debt Evolution in France

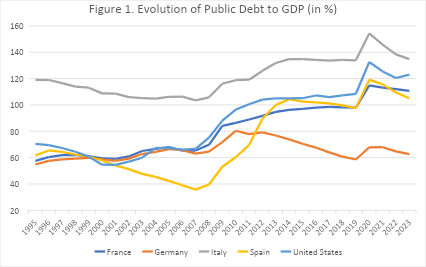

Political uncertainty is particularly damaging when viewed against France's private debt situation. Data from the IMF's Global Debt Monitor, compared to Germany, Spain, the U.S., and Italy, reveals striking trends. Public debt as a percentage of GDP has risen significantly in Spain, the U.S., France, and Italy since the 2008 financial crisis, while Germany has bucked this trend (see Figure 1). In 2023, France's public debt-to-GDP ratio stood at 111%, compared to 123% in the U.S. and 135% in Italy.

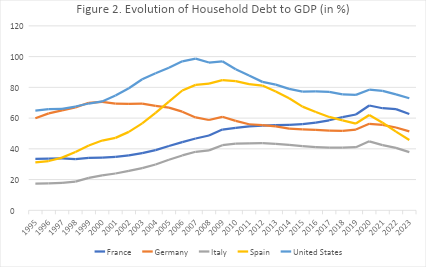

In terms of household debt, including loans and debt securities, the U.S. leads with 73% of GDP, while France follows at 63% (see Figure 2). Notably, Spain has significantly reduced household debt from 85% of GDP in 2009 to 46% in 2023.

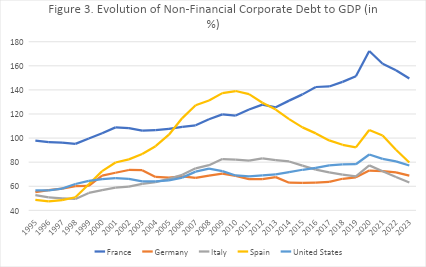

Regarding non-financial corporate debt, France presents the highest levels among the observed countries, with debt reaching 150% of GDP in 2023 (see Figure 3). Spain ranks second at 80%, but it has achieved significant deleveraging since 2010, when corporate debt stood at 139% of GDP. France is the only country where non-financial corporate debt has notably increased since the financial crisis. While all countries have reduced debt levels since 2020, much of this reduction relates to the repayment of COVID-19-related financial support.

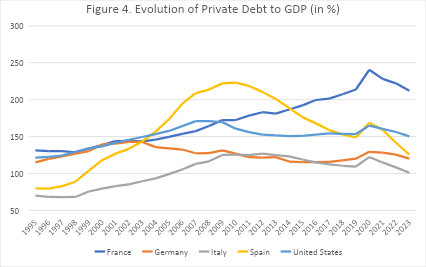

Private debt, combining household and corporate debt, reveals France's elevated levels, totaling 212% of GDP in 2023 (see Figure 4). Adding public debt, which stands at 111%, underscores that the current political crisis comes at an inopportune time. Prolonged gridlock could hinder necessary reforms. A society with high levels of debt faces a dual challenge: on one hand, it has a greater risk of experiencing a financial crisis, as debt obligations can become unsustainable in the face of unexpected economic changes. On the other hand, such a society has less capacity to anticipate and effectively respond to these risks, as both public and private maneuvering room is significantly reduced. In the case of France, this vulnerability is exacerbated by the current political weakness of the government, which hinders the implementation of decisive measures to stabilize the economy, such as structural reforms or budget adjustments. This combination of high debt levels and political fragility not only increases the risk of a crisis but also limits the tools available to prevent or mitigate its impact.

The Situation of France's Three Major Banks

The economic and political turmoil in France is also impacting its three largest banks. BNP Paribas has slipped from the Top 3 in European bank market capitalization, now ranking fourth behind HSBC, Santander, and Intesa.

Situation of the Three Largest French Banks.

| Bank | Market Capitalization (million €) | NPL/Loans (%) | Senior CDS | CDS Subordinated |

|---|---|---|---|---|

| BNP PARIBAS | 66,067 | 2.17 | 47.04 | 101.78 |

| CRÉDIT AGRICOLE | 39,629 | 1.24 | 44.66 | 103.89 |

| SOCIÉTÉ GÉNÉRALE | 20,776 | 3.38 | 52.44 | 133.47 |

| Bank | Price-to-Book | ROE (%) | ROA (%) | Efficiency Ratio (%) |

| BNP PARIBAS | 0.51 | 9.31 | 0.44 | 60.4 |

| CRÉDIT AGRICOLE | 0.54 | 9.73 | 0.34 | 56.4 |

| SOCIÉTÉ GÉNÉRALE | 0.29 | 8.28 | 0.40 | 63.3 |

Data as of 12/6/2024. Source: Capital IQ. NPL/L: Non-Performing Loans as a Percentage of Total Loans in the Last Quarter; CDS Senior: Credit Default Swap on Senior Bank Debt in Basis Points; CDS Subordinated: Credit Default Swap on Subordinated Bank Debt in Basis Points; ROE: Annualized Return on Equity for the Last Quarter; ROA: Annualized Return on Assets for the Last Quarter; Efficiency Ratio: Operating Expenses/Gross Margin.

Non-Performing Loans (NPLs) remain at manageable levels. CDS for senior and subordinated debt of the three French banks are comparable to those of their competitors. However, low profitability, as measured by Return on Equity (ROE) and Return on Assets (ROA), coupled with high efficiency ratios (operating costs relative to revenues), undermines market valuations. Société Générale, in particular, has a notably low price-to-book ratio.

In France, fixed-rate loans dominate. Société Générale's 2023 annual report shows that 67.40% of its loan portfolio consists of fixed-rate loans. Consequently, interest rate hikes in 2022 and 2023 have negatively impacted the valuation of French banks. Additionally, consumer protection policies in France have hindered bank profitability. For instance, when the 12-month Euribor turned negative in February 2016, French fixed-rate mortgage loans were renegotiated. By January 2017, 61.6% of these loans had been renegotiated, according to the Bank of France.

This dynamic negatively impacted the sector's profitability and created instability. While lower interest rates trigger renegotiations, higher rates cause latent market value losses on fixed-rate loans without equivalent renegotiation. Excessive consumer protection can harm company valuations and reduce their capacity to contribute positively to the economy-a lesson Europe must heed.

Rising yields on French 10-year bonds (now at 2.88%) have also eroded the market value of bonds held by banks. While the situation is not yet critical, as the spread with German bonds remains modest (2.88%-2.12%), the ECB's Transmission Protection Instrument (TPI), introduced in July 2022, serves as a safeguard against potential fragmentation in the Eurozone. Investors are reassured that the ECB would act if French bond yields surged, alleviating pressure on banks.

Conclusion: Resilience Amid Uncertainty

The level of indebtedness of non-financial companies in France impacts French banks, but the country's major banks have consistently demonstrated resilience. However, a weak French government that is unable to implement necessary structural reforms, budget adjustments, and measures to promote corporate investment would diminish the banks' ability to cope with a worsening economic situation. For the Eurozone, it is crucial that French banks improve their profitability, as this is the best guarantee for economic development, social well-being, and the ability to provide financing to businesses, households, and the country as a whole.